Summary

Electricity in Europe may be 10x more expensive than it was a year ago, but savvy clean energy buyers can still strike good deals and make progress on their clean energy goals if they know where to look and how to negotiate.

Over the past year, the global renewable energy industry has faced several unexpected challenges, creating a volatile market environment for buyers and sellers alike.

But Europe’s heightened determination to achieve energy independence from Russia is increasing corporate and government demand for renewables, encouraging flexibility on both sides of the table, and ultimately carrying the European clean energy market through these turbulent times. For clean energy buyers in Europe, there are viable options, but conditions vary greatly between countries.

Here, we will review the effect of market forces on pricing and project availability and what corporate buyers can do to successfully transact in Europe.

Background: Europe Faces Historically High Electricity Prices

Unusual circumstances strain natural gas supply

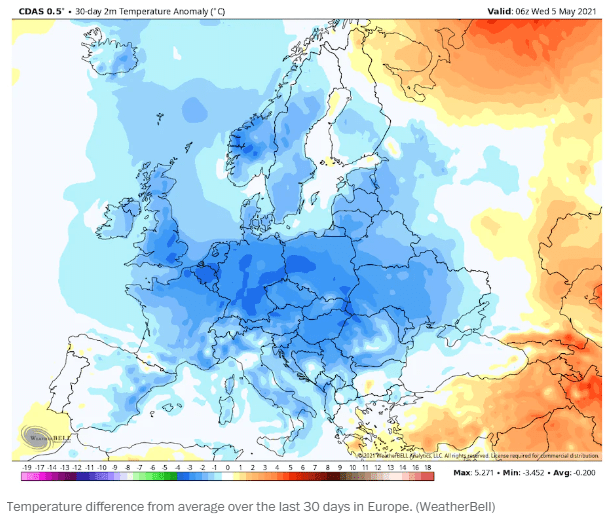

The rise of wholesale electricity prices can be traced back to 2020. While the previous 2019-2020 winter season was one of the warmest on record, the 2020-2021 winter season brought arctic weather conditions across northern and central Europe. The UK saw its coldest average low temperature since 1922 and all of Europe since 2003. This very cold weather raised demand for heating, requiring the use of an already limited supply of natural gas reserves.

As the winter months tailed off, COVID restrictions eased and businesses reopened their doors, raising energy demand to pre-COVID levels.

In a normal market environment, these events would trigger additional imports of natural gas, but that didn’t occur because the EU was competing with the rest of the world which was also increasing its natural gas consumption.

High demand and low supply made natural gas more expensive, which in turn made electricity produced by natural gas more expensive.

To make matters worse, wind power generation from operating wind farms was at an all-time low across Europe due to unusually low average wind speed.

By June 2021, electricity prices broke the 100 Euro/MWh mark across most of Europe. Prices continued to skyrocket for the remainder of the year, ending over 300 Euro/MWh.

The Russo-Ukrainian war is keeping natural gas expensive and scarce

In 2022, the Russo-Ukrainian War has only fueled more market volatility. Europe typically gets over 40% of its natural gas supply from Russia. The European Commission has asked over 20 European countries to reduce their natural gas consumption by at least 15% until next April 2023 to account for unplanned cutoffs from Russia and to transition the continent to energy independence—now a geopolitical priority.

Greenpeace activists protest Polish imports of Russian oil, March 2022

Source: Flickr/Greenpeace Polska

The other, somewhat more controversial, emergency measure being discussed by the European Commission is placing a potential price cap on natural gas. However, countries are divided on whether to impose a cap on natural gas, and if it would exacerbate rather than ease Europe’s energy crisis.

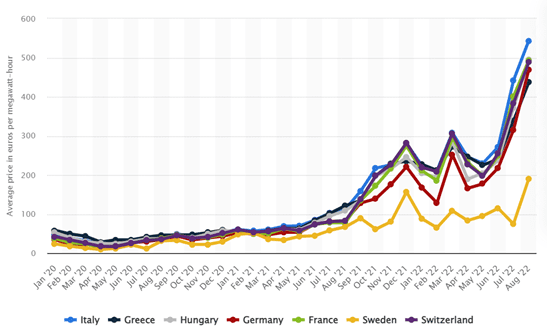

Today, average monthly wholesale electricity prices are over 10 times what they were one year ago.

European PPA Economics Have Changed, But Are Manageable

Power Purchase Agreements (PPAs) are the most common way that large organizations buy clean energy. In a PPA, a corporate buyer pays a fixed monthly price to a wind or solar project developer. In exchange, the buyer receives the floating market rate of the electricity generated by that project and sold to the grid, plus Guarantees of Origin (GOs). For a refresher on how PPAs work, read our blog on PPAs.

The good news: the floating market rate—a source of risk for PPA buyers—is likely to remain elevated in coming years, driving higher economic value for PPAs starting in the near-term.

The bad news: the average solar and wind PPA fixed price offers are also high—up about 45% since 2021.

Developers are likely to keep the fixed price of wind and solar projects elevated in the foreseeable future for several reasons.

First, developers expect electricity to stay expensive in coming years as Europe’s energy landscape shapes itself into a cleaner, more independent grid at a much faster pace than originally planned. This will encourage developers to keep PPA prices elevated to ensure an expected financial return like that of other selling options developers may be able to explore on the merchant market.

Second, demand isn’t going away. Companies are continuing to set ambitious climate goals and now they have an even bigger competitor in town: governments, which are often favored by developers for their extremely low default risk.

Third, let’s not forget ongoing supply chain constraints and increased commodity prices for materials used in solar panels or wind turbines.

How and Where to Find Good Deals

Some markets are better than others. Spain, Sweden, and Finland in particular have better price stability and resilience to market volatility. Spain has strong competition and is prime for solar, with some of the highest levels of irradiance throughout Europe. Sweden and Finland’s PPA prices remain stable for different reasons, largely due to low interconnection costs and supportive regulations.

Market conditions in other European countries will likely improve now that those governments have more “skin in the game.” Several European countries are resolving long-standing project development obstacles such as land use permitting uncertainties and back-logged interconnection queues.

In May, the European Commission released guidelines through their REPowerEU Plan for fast-tracking the permitting process to one year in member states that dedicate “go-to” areas for renewables. Germany, for example, is already working towards reserving 2% of land for wind farms by 2032 to capitalize on a quicker permitting process.

Bottom Line: Prepared Buyers Can Succeed in This Market

Corporate buyers who have transacted within the past year report that innovative contract structures, flexibility in commercial operation date and pricing mechanisms, and exhaustive project due diligence are key aspects of dealing with current market and regulatory uncertainty. Experienced buyers that have previously negotiated through these various types of “new” and innovative structures will have a leg up on those transacting for the first time.

It is also important that you approach this market with strong internal alignment. Procurement leaders should know where their organization can be flexible and where they have hard limitations. Developers will favor prepared counterparties with a fast path to a done deal.

One thing is certain: Europe’s renewable energy transition is shifting into high gear. Corporate buyers can position themselves favorably by being ready to act strategically and efficiently.

Coho Climate Advisors LLC (“Coho”) is registered with the U.S. Commodity Futures Trading Commission as a commodity trading advisor and is a member of the National Futures Association (NFA ID: 0542152). Information in this article is provided for general informational purposes only and should not be considered legal or commodity trading advice or as forming the basis of any advisory relationship with Coho. Trading in commodity interests and financially settled energy contracts, such as virtual power purchase agreements, can be complex and involves risk of loss that can be substantial. At a minimum, you should consult with your own legal and accounting advisors in considering whether to enter into any such contract.